Affordable single-family home construction company LGI Homes (NASDAQ:LGIH) will be announcing earnings results tomorrow before the bell. Here’s what you need to know.

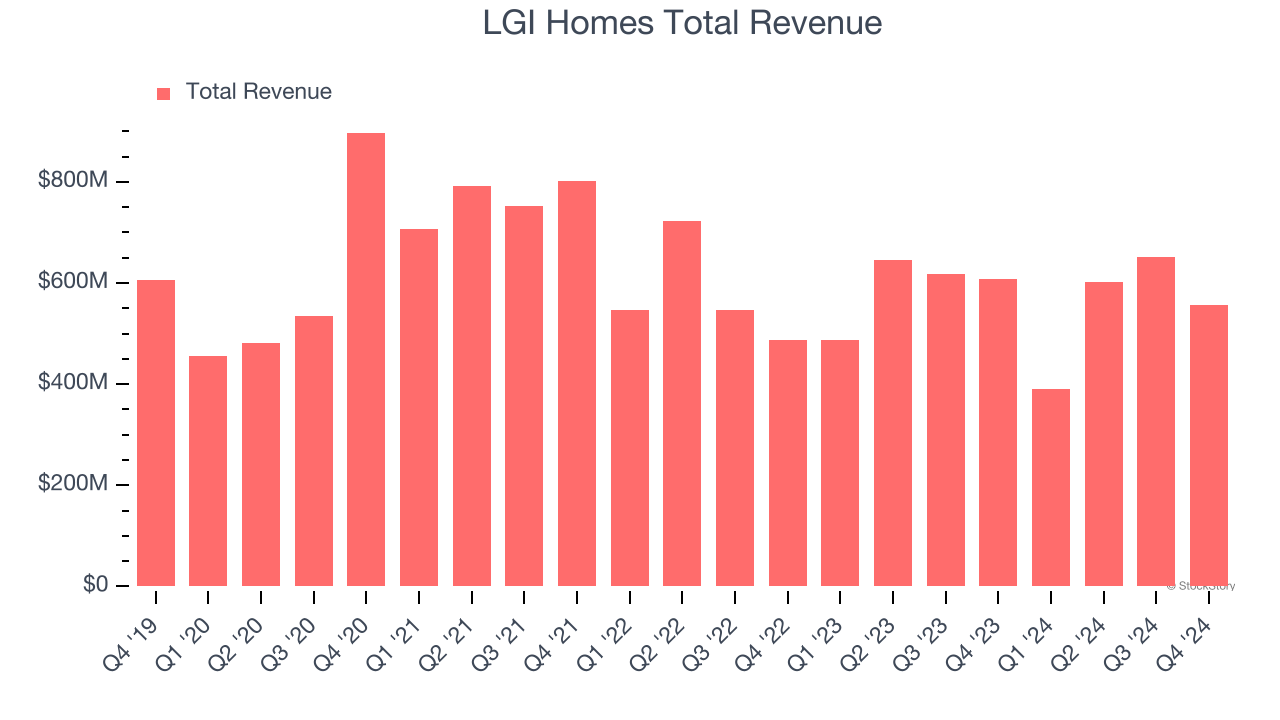

LGI Homes missed analysts’ revenue expectations by 11% last quarter, reporting revenues of $557.4 million, down 8.4% year on year. It was a disappointing quarter for the company, with a significant miss of analysts’ adjusted operating income estimates.

Is LGI Homes a buy or sell going into earnings? Read our full analysis here, it’s free.

This quarter, analysts are expecting LGI Homes’s revenue to decline 5.3% year on year to $370.1 million, improving from the 19.8% decrease it recorded in the same quarter last year. Adjusted earnings are expected to come in at $0.63 per share.

Analysts covering the company have generally reconfirmed their estimates over the last 30 days, suggesting they anticipate the business to stay the course heading into earnings. LGI Homes has missed Wall Street’s revenue estimates five times over the last two years.

Looking at LGI Homes’s peers in the home builders segment, some have already reported their Q1 results, giving us a hint as to what we can expect. Taylor Morrison Home delivered year-on-year revenue growth of 11.5%, beating analysts’ expectations by 5.7%, and Tri Pointe Homes reported a revenue decline of 21.1%, topping estimates by 4%. Taylor Morrison Home traded down 1.1% following the results while Tri Pointe Homes was also down 1.6%.

Read our full analysis of Taylor Morrison Home’s results here and Tri Pointe Homes’s results here.

Investors in the home builders segment have had fairly steady hands going into earnings, with share prices down 1.4% on average over the last month. LGI Homes is down 9.7% during the same time and is heading into earnings with an average analyst price target of $106.67 (compared to the current share price of $60.05).

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.