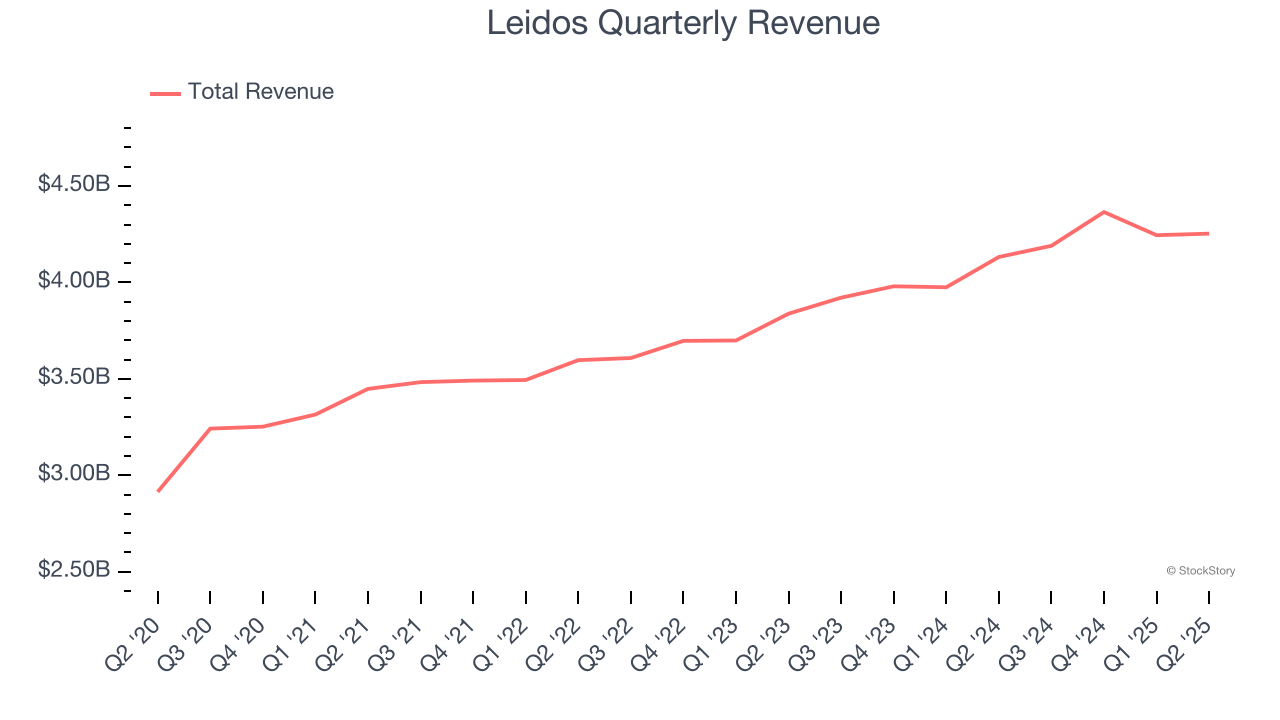

Defense contractor Leidos (NYSE:LDOS) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 2.9% year on year to $4.25 billion. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $17.1 billion at the midpoint. Its non-GAAP profit of $3.21 per share was 20.9% above analysts’ consensus estimates.

Is now the time to buy Leidos? Find out by accessing our full research report, it’s free.

Leidos (LDOS) Q2 CY2025 Highlights:

- Revenue: $4.25 billion vs analyst estimates of $4.25 billion (2.9% year-on-year growth, in line)

- Adjusted EPS: $3.21 vs analyst estimates of $2.65 (20.9% beat)

- Adjusted EBITDA: $647 million vs analyst estimates of $546.1 million (15.2% margin, 18.5% beat)

- The company reconfirmed its revenue guidance for the full year of $17.1 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $10.55 at the midpoint

- Operating Margin: 13.4%, up from 11.5% in the same quarter last year

- Free Cash Flow Margin: 10.7%, up from 8.5% in the same quarter last year

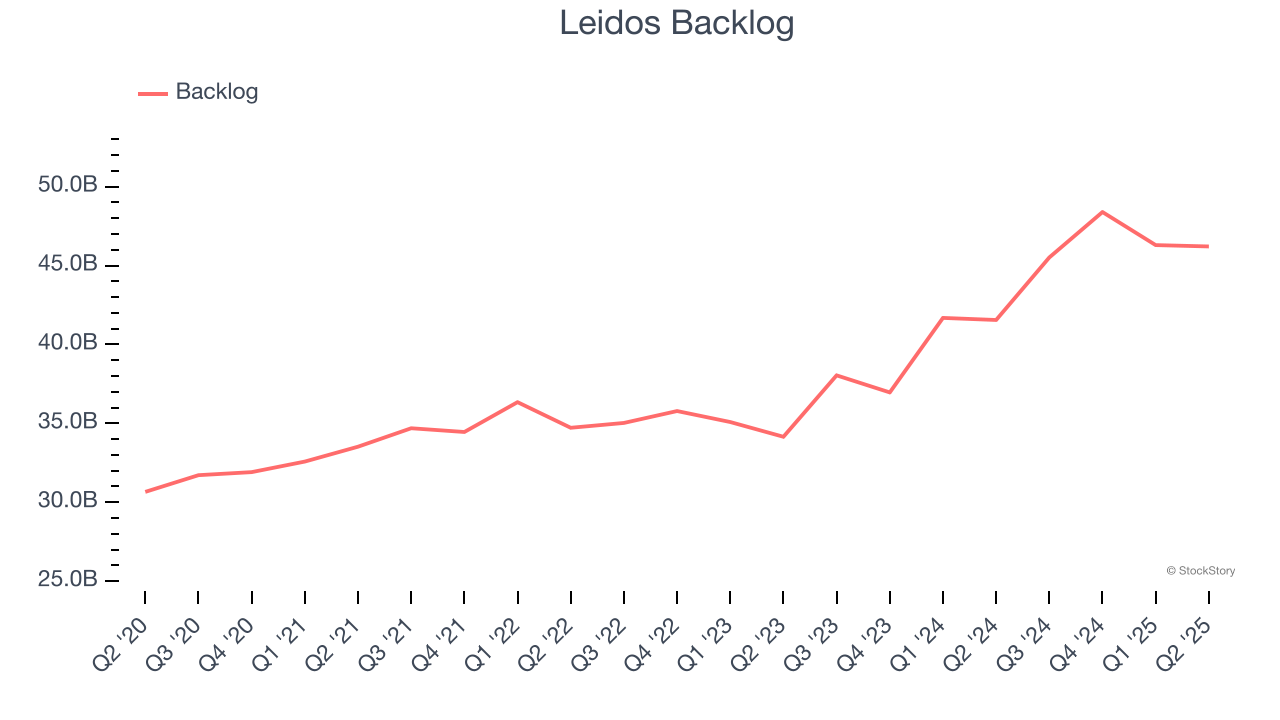

- Backlog: $46.21 billion at quarter end, up 11.2% year on year

- Market Capitalization: $20.72 billion

"Our second quarter results showcase the strength of our differentiated portfolio and the alignment of our NorthStar 2030 strategy with the priorities of the new Administration," said Leidos Chief Executive Officer Tom Bell.

Company Overview

Formed through the split of IT services company SAIC, Leidos (NYSE:LDOS) offers technology and engineering solutions such as military training systems for the defense, civil, and health markets.

Revenue Growth

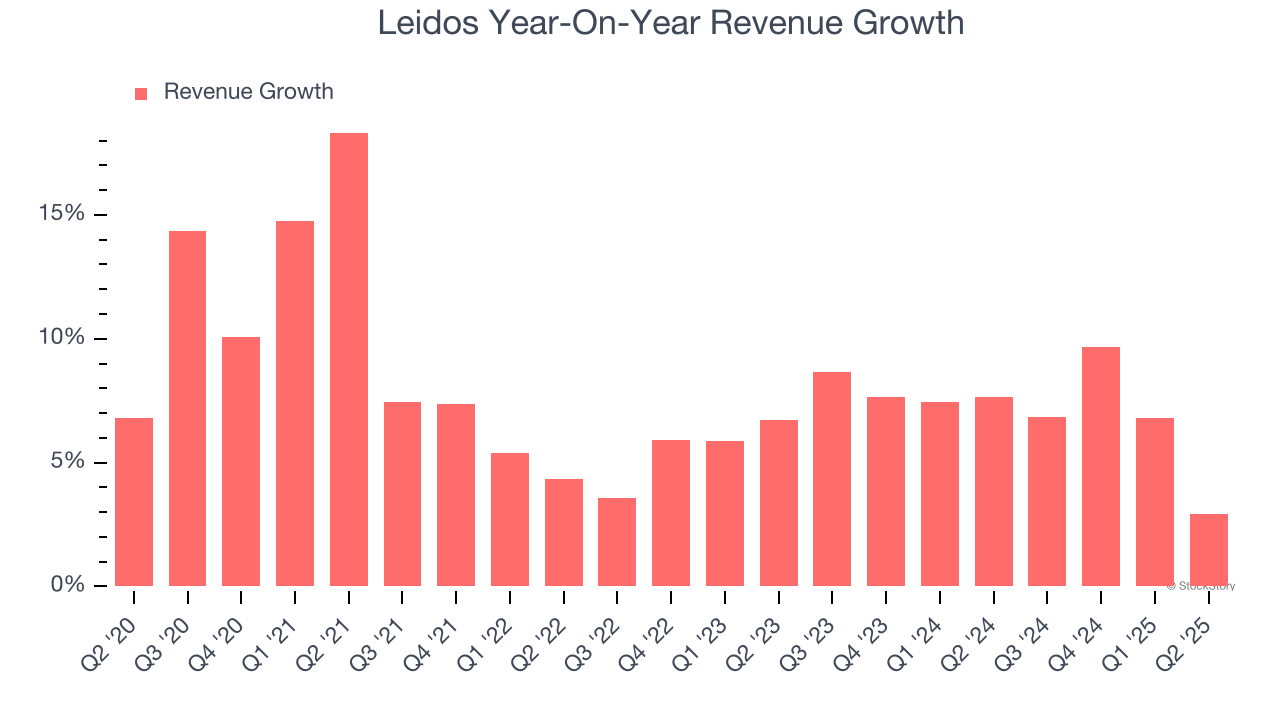

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Leidos’s sales grew at a decent 8% compounded annual growth rate over the last five years. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Leidos’s annualized revenue growth of 7.2% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Leidos’s backlog reached $46.21 billion in the latest quarter and averaged 15.7% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Leidos’s products and services but raises concerns about capacity constraints.

This quarter, Leidos grew its revenue by 2.9% year on year, and its $4.25 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Leidos has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.4%, higher than the broader industrials sector.

Looking at the trend in its profitability, Leidos’s operating margin rose by 3.4 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q2, Leidos generated an operating margin profit margin of 13.4%, up 1.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

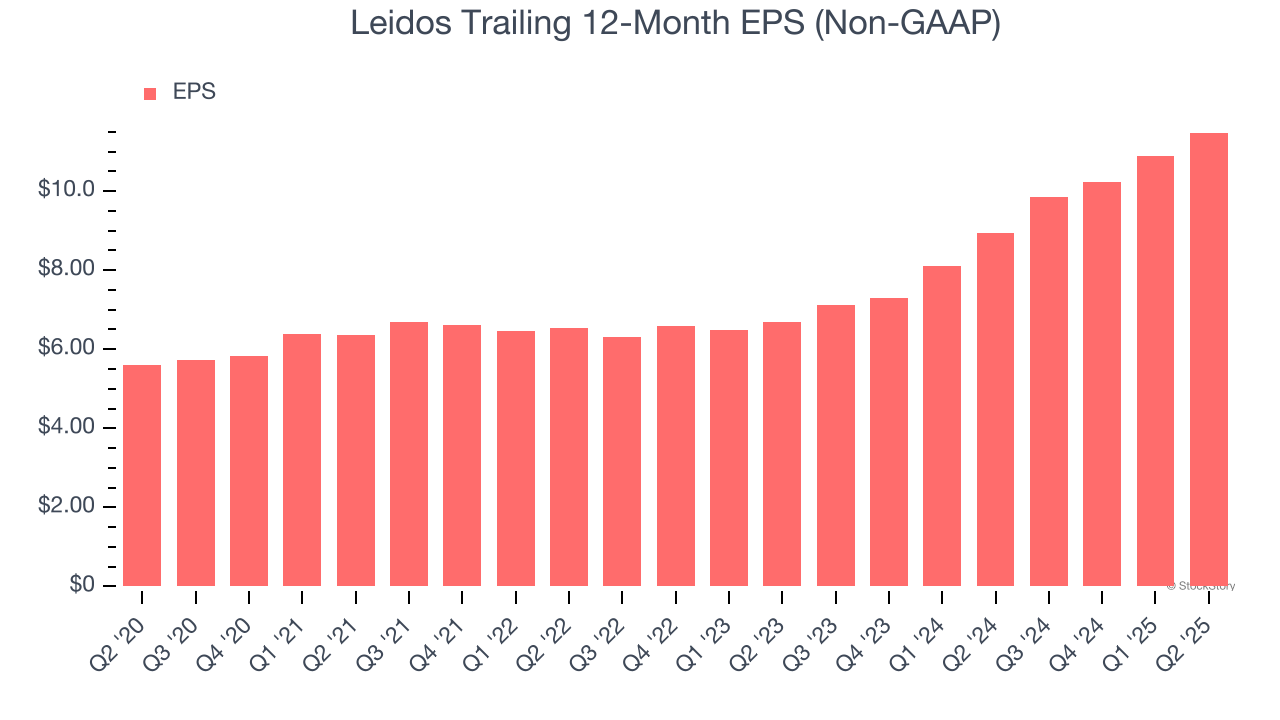

Leidos’s EPS grew at a spectacular 15.4% compounded annual growth rate over the last five years, higher than its 8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

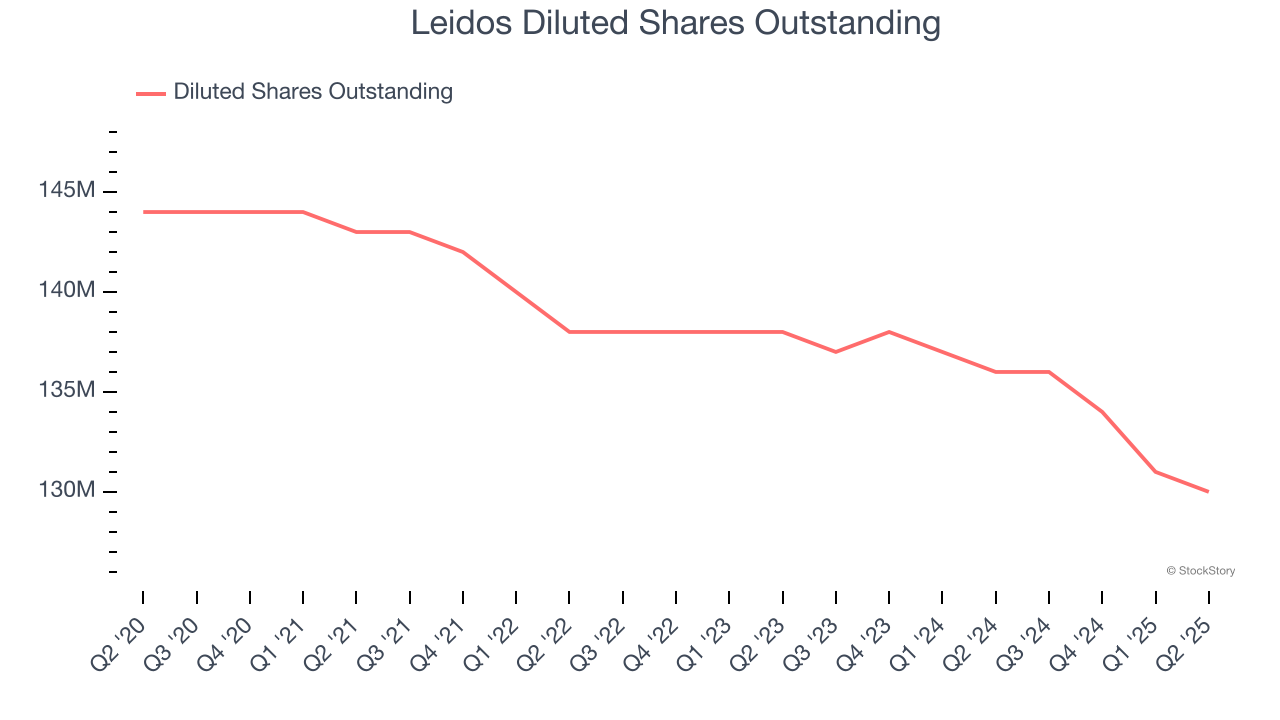

Diving into Leidos’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Leidos’s operating margin expanded by 3.4 percentage points over the last five years. On top of that, its share count shrank by 9.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Leidos, its two-year annual EPS growth of 31% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q2, Leidos reported adjusted EPS at $3.21, up from $2.63 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Leidos’s full-year EPS of $11.48 to shrink by 3.8%.

Key Takeaways from Leidos’s Q2 Results

We were impressed by how significantly Leidos blew past analysts’ backlog expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EPS guidance missed and its full-year revenue guidance was in line with Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 5.7% to $170.50 immediately following the results.

Indeed, Leidos had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.