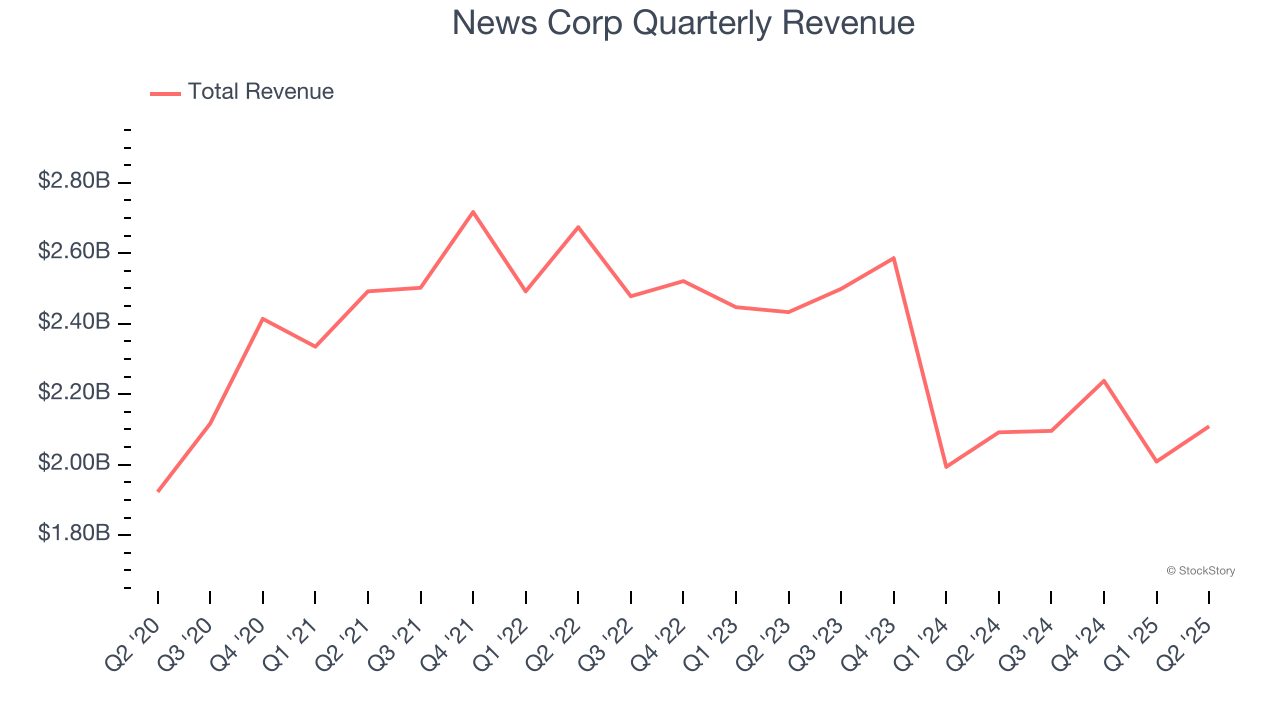

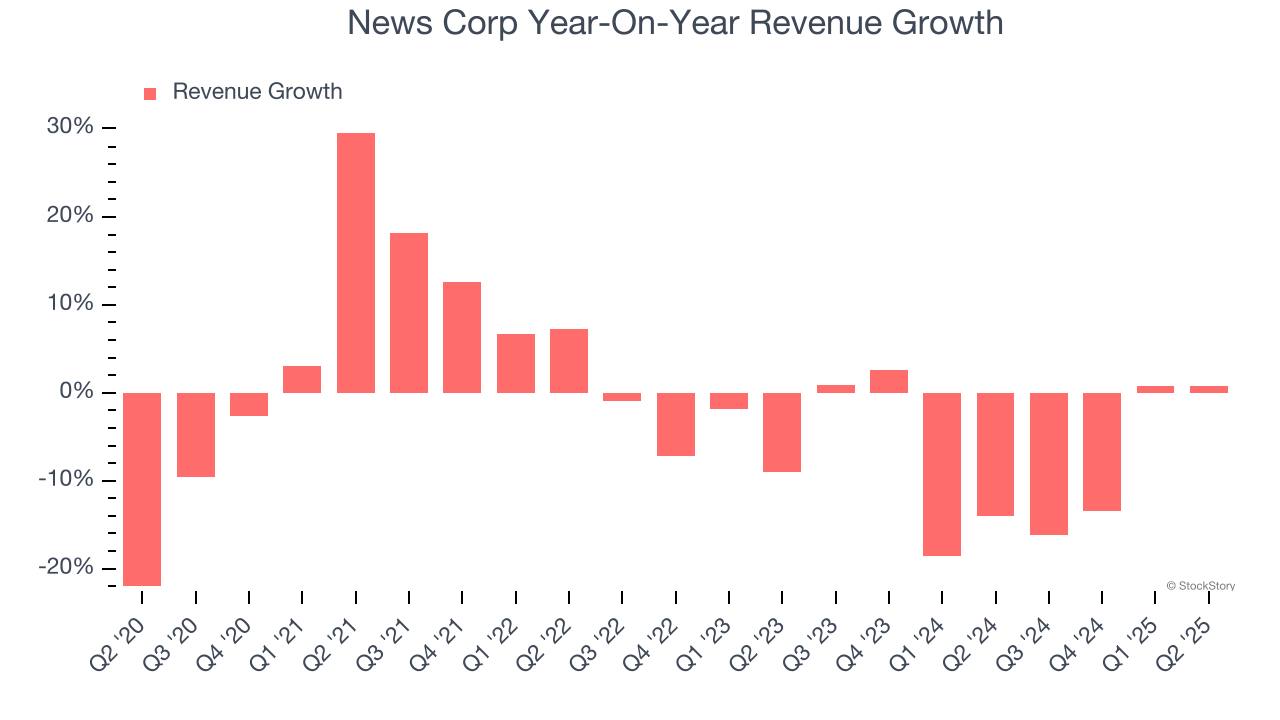

Global media and publishing company News Corp (NASDAQ:NWSA) reported Q2 CY2025 results beating Wall Street’s revenue expectations, but sales were flat year on year at $2.11 billion. Its non-GAAP profit of $0.89 per share was significantly above analysts’ consensus estimates.

Is now the time to buy News Corp? Find out by accessing our full research report, it’s free.

News Corp (NWSA) Q2 CY2025 Highlights:

- Revenue: $2.11 billion vs analyst estimates of $2.09 billion (flat year on year, 1% beat)

- Adjusted EPS: $0.89 vs analyst estimates of $0.18 (significant beat)

- Adjusted EBITDA: $329 million vs analyst estimates of $312.4 million (15.6% margin, 5.3% beat)

- Operating Margin: 6.5%, down from 9% in the same quarter last year

- Free Cash Flow Margin: 1.5%, down from 5.3% in the same quarter last year

- Market Capitalization: $17.36 billion

Company Overview

Established in 2013 after a restructuring, News Corp (NASDAQ:NWSA) is a multinational conglomerate known for its news publishing, broadcasting, digital media, and book publishing.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, News Corp’s demand was weak and its revenue declined by 1.3% per year. This was below our standards and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. News Corp’s recent performance shows its demand remained suppressed as its revenue has declined by 7.5% annually over the last two years.

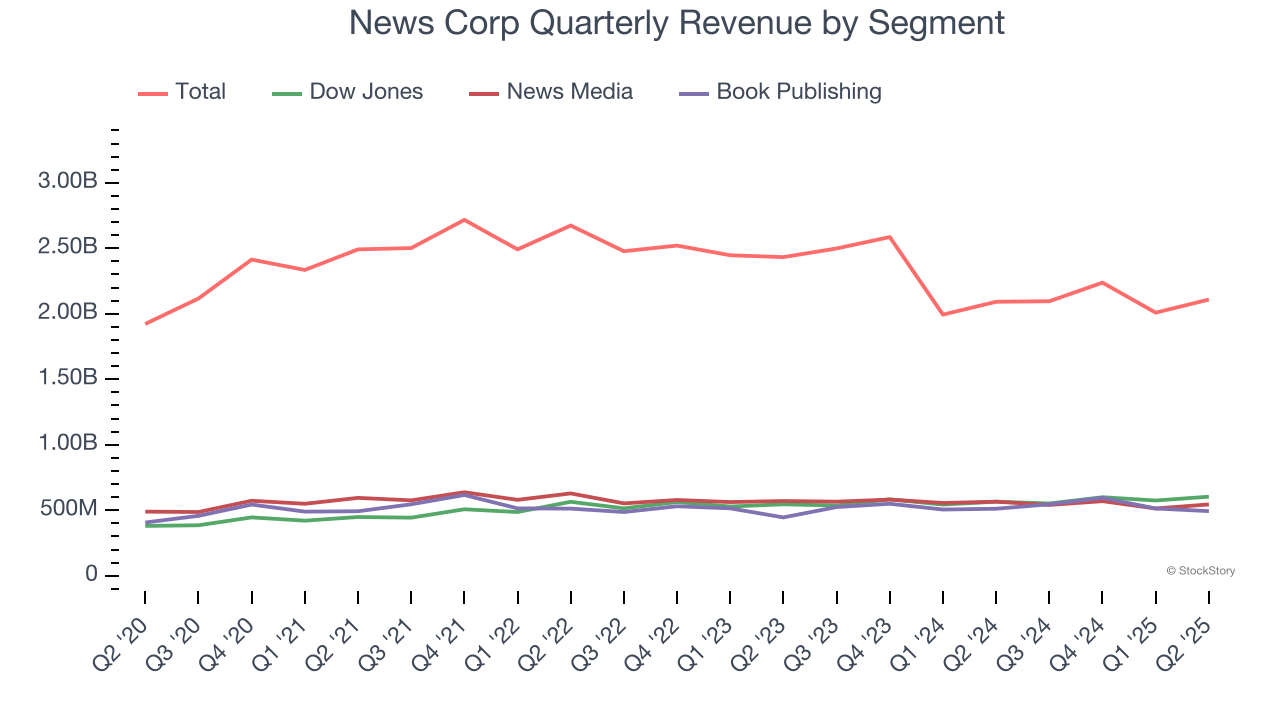

News Corp also breaks out the revenue for its three most important segments: Dow Jones, News Media, and Book Publishing, which are 28.6%, 25.8%, and 23.4% of revenue. Over the last two years, News Corp’s Dow Jones (media subsidiary) and Book Publishing (general publishing) revenues averaged year-on-year growth of 4.1% and 4.3%. On the other hand, its News Media revenue (general media) averaged 2.1% declines.

This quarter, News Corp’s $2.11 billion of revenue was flat year on year but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

News Corp’s operating margin has risen over the last 12 months and averaged 9.7% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports mediocre profitability for a consumer discretionary business.

In Q2, News Corp generated an operating margin profit margin of 6.5%, down 2.5 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

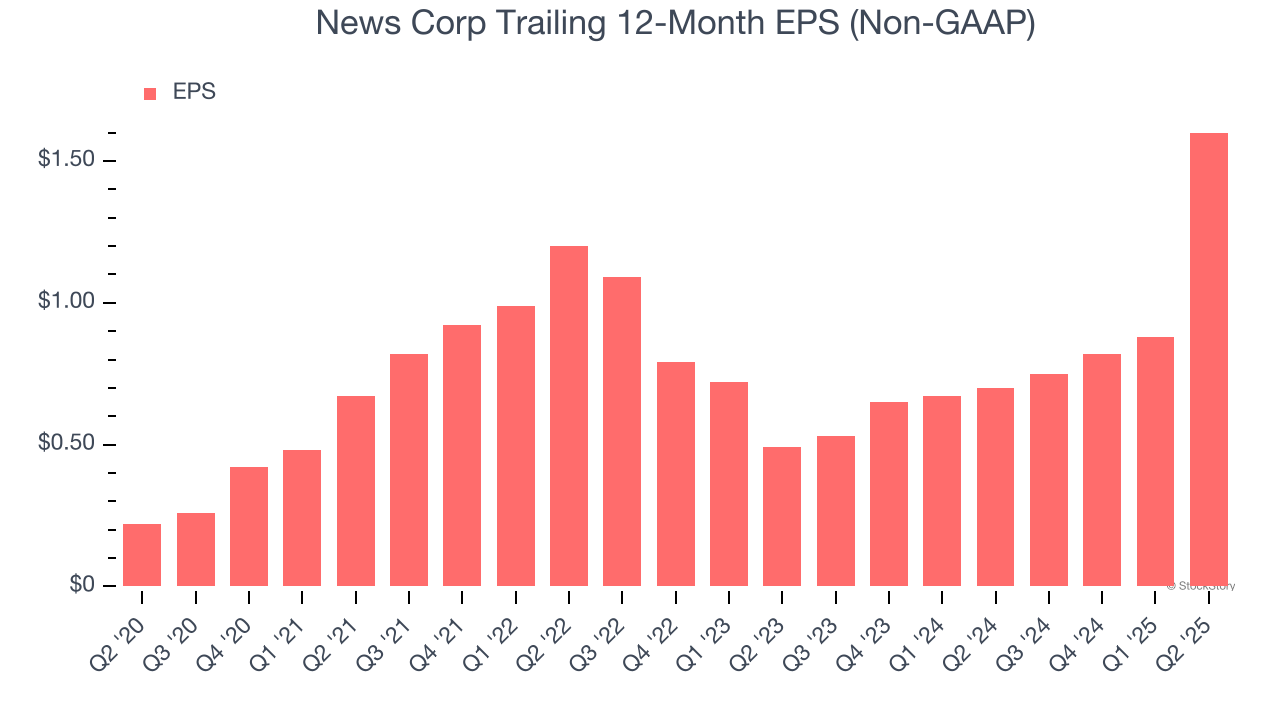

News Corp’s EPS grew at an astounding 48.7% compounded annual growth rate over the last five years, higher than its 1.3% annualized revenue declines. This tells us management adapted its cost structure in response to a challenging demand environment.

In Q2, News Corp reported adjusted EPS at $0.89, up from $0.17 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects News Corp’s full-year EPS of $1.60 to shrink by 38.5%.

Key Takeaways from News Corp’s Q2 Results

We were impressed by how significantly News Corp blew past analysts’ EPS expectations this quarter. We were also happy its revenue and EBITDA outperformed Wall Street’s estimates despite the miss in its News Media segment. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $29.51 immediately after reporting.

News Corp put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.