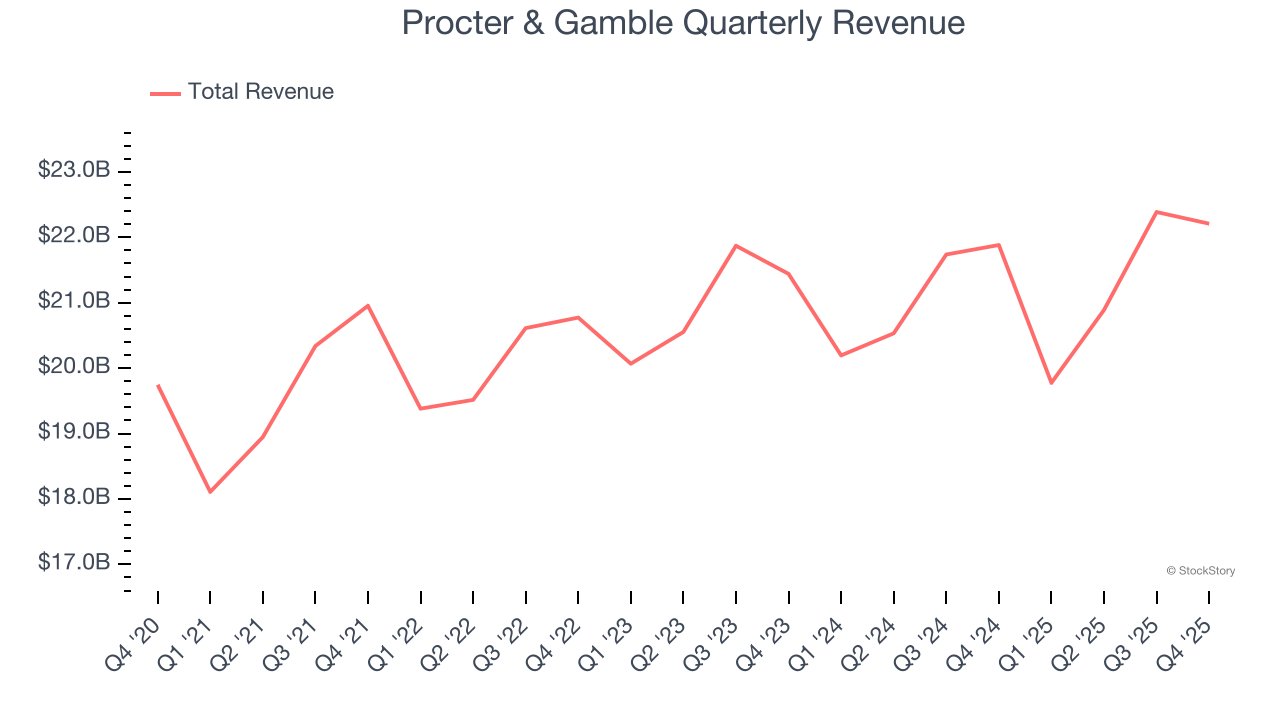

Consumer products behemoth Proctor & Gamble (NYSE:PG) met Wall Streets revenue expectations in Q4 CY2025, with sales up 1.5% year on year to $22.21 billion. Its non-GAAP profit of $1.88 per share was 1.2% above analysts’ consensus estimates.

Is now the time to buy Procter & Gamble? Find out by accessing our full research report, it’s free.

Procter & Gamble (PG) Q4 CY2025 Highlights:

- Revenue: $22.21 billion vs analyst estimates of $22.29 billion (1.5% year-on-year growth, in line)

- Adjusted EPS: $1.88 vs analyst estimates of $1.86 (1.2% beat)

- Adjusted EBITDA: $6.39 billion vs analyst estimates of $6.46 billion (28.8% margin, 1% miss)

- Management reiterated its full-year Adjusted EPS guidance of $6.96 at the midpoint

- Operating Margin: 24.2%, down from 27.2% in the same quarter last year

- Free Cash Flow Margin: 17.1%, similar to the same quarter last year

- Organic Revenue was flat year on year

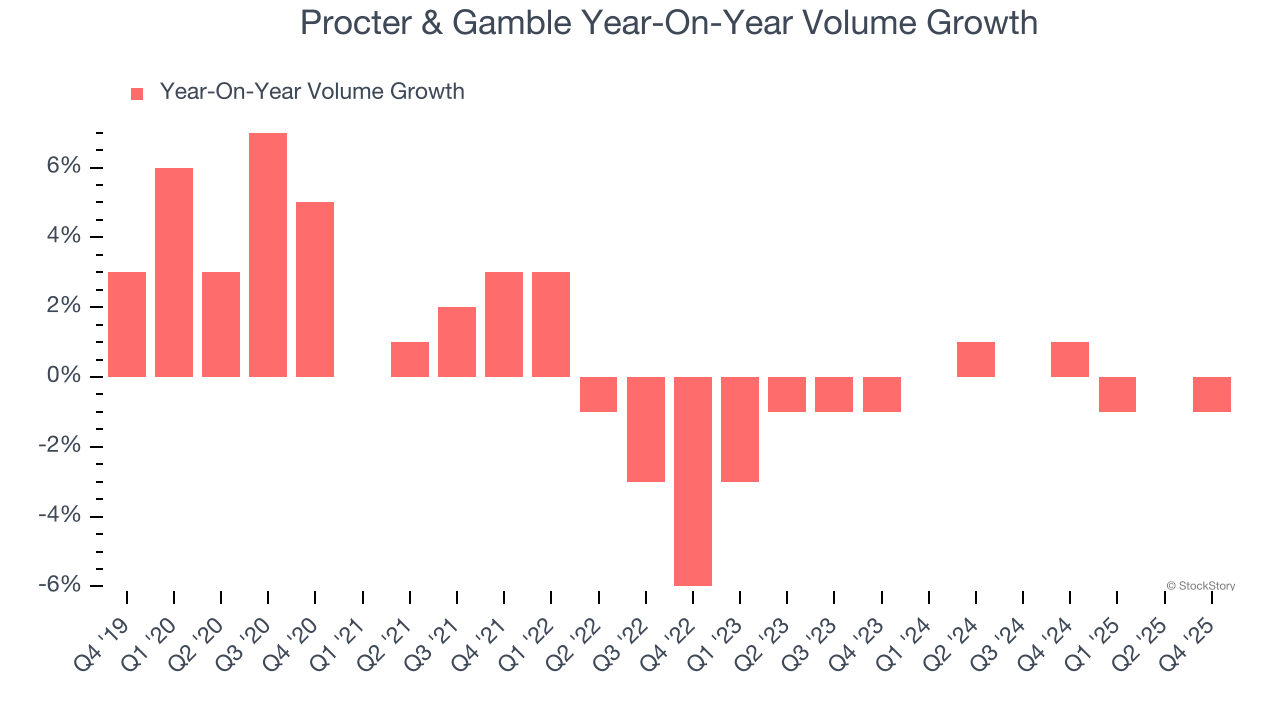

- Sales Volumes fell 1% year on year (1% in the same quarter last year)

- Market Capitalization: $341.3 billion

“Our results in the second quarter keep us on track to deliver within our fiscal year guidance ranges for organic sales growth, core EPS growth and adjusted free cash flow productivity in a challenging consumer and geopolitical environment,” said Shailesh Jejurikar, President and Chief Executive Officer.

Company Overview

Founded by candle maker William Procter and soap maker James Gamble, Proctor & Gamble (NYSE:PG) is a consumer products behemoth whose product portfolio spans everything from facial tissues to laundry detergent to feminine care to men’s grooming.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $85.26 billion in revenue over the past 12 months, Procter & Gamble is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To expand meaningfully, Procter & Gamble likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, Procter & Gamble grew its sales at a sluggish 2% compounded annual growth rate over the last three years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Procter & Gamble grew its revenue by 1.5% year on year, and its $22.21 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months, similar to its three-year rate. While this projection indicates its newer products will fuel better top-line performance, it is still below the sector average.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Procter & Gamble’s quarterly sales volumes have, on average, stayed about the same over the last two years. This stability is normal because the quantity demanded for consumer staples products typically doesn’t see much volatility.

In Procter & Gamble’s Q4 2026, sales volumes dropped 1% year on year.

Key Takeaways from Procter & Gamble’s Q4 Results

We struggled to find many positives in these results. Volumes shrank year-on-year. Its gross margin missed and EBITDA also both fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 1.9% to $143.31 immediately after reporting.

Big picture, is Procter & Gamble a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).