Student loan provider Sallie Mae (NASDAQ:SLM) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 16.4% year on year to $454.1 million. Its GAAP profit of $1.12 per share was 19.7% above analysts’ consensus estimates.

Is now the time to buy Sallie Mae? Find out by accessing our full research report, it’s free.

Sallie Mae (SLM) Q4 CY2025 Highlights:

- Net Interest Income: $377.1 million vs analyst estimates of $381.9 million

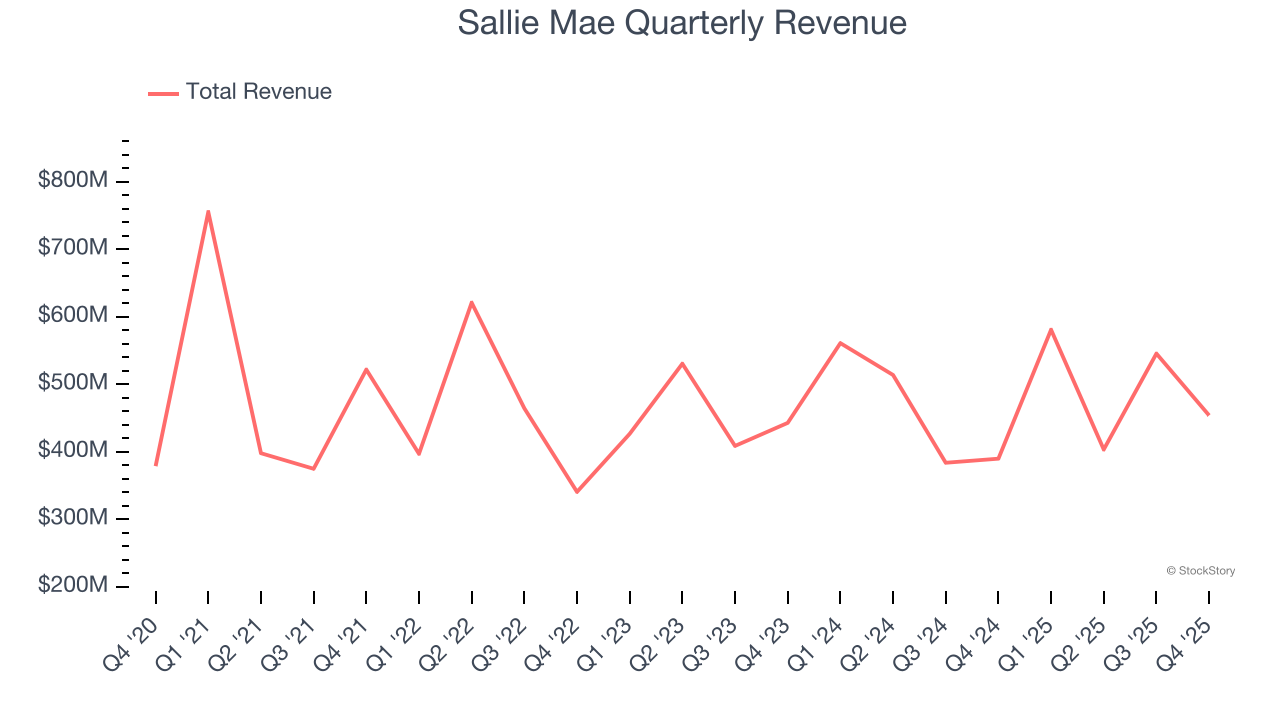

- Revenue: $454.1 million vs analyst estimates of $449.7 million (16.4% year-on-year growth, 1% beat)

- Pre-tax Profit: $316 million (69.6% margin)

- EPS (GAAP): $1.12 vs analyst estimates of $0.94 (19.7% beat)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $2.75 at the midpoint, missing analyst estimates by 1%

- Market Capitalization: $5.37 billion

Company Overview

Originally created as a government-sponsored enterprise before privatizing in 2004, Sallie Mae (NASDAQ:SLM) is a financial services company that provides private education loans, savings products, and educational resources to help students and families pay for college.

Revenue Growth

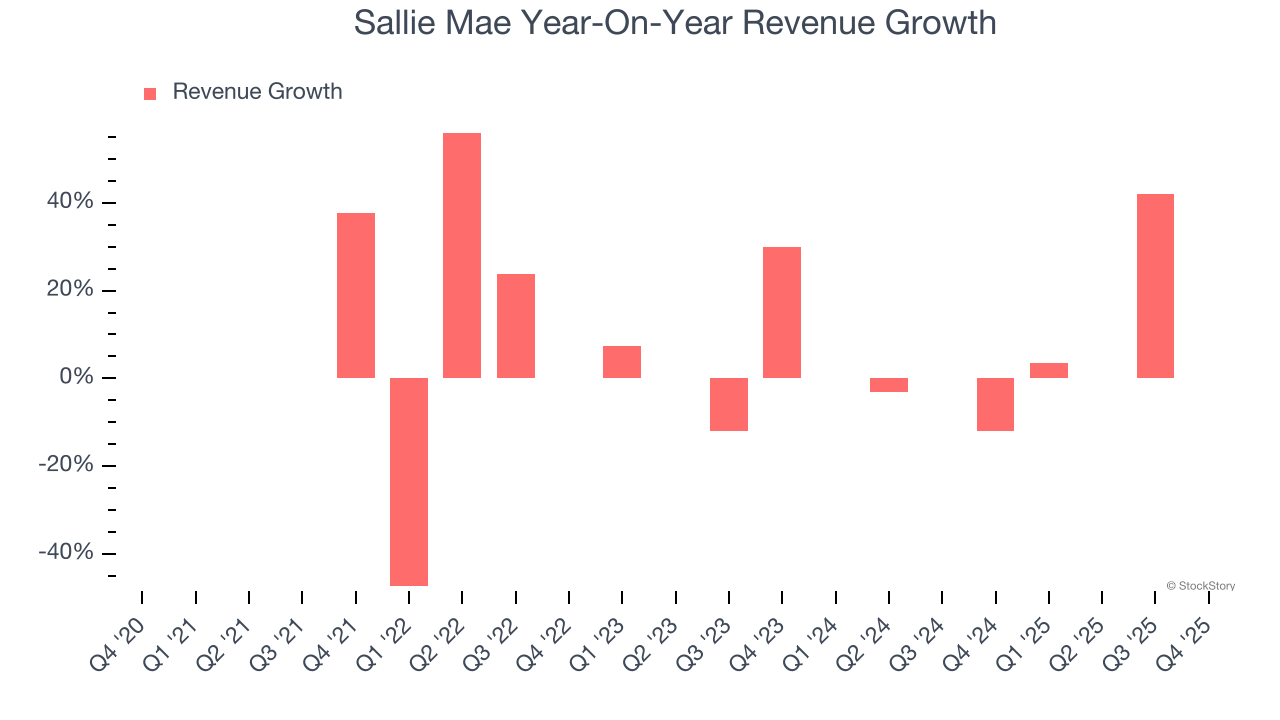

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Sallie Mae’s 2% annualized revenue growth over the last five years was sluggish. This wasn’t a great result, but there are still things to like about Sallie Mae.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Sallie Mae’s annualized revenue growth of 4.7% over the last two years is above its five-year trend, but we were still disappointed by the results.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Sallie Mae reported year-on-year revenue growth of 16.4%, and its $454.1 million of revenue exceeded Wall Street’s estimates by 1%.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Key Takeaways from Sallie Mae’s Q4 Results

It was good to see Sallie Mae beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its net interest income slightly missed and its full-year EPS guidance fell slightly short of Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 4.3% to $27.86 immediately following the results.

Sallie Mae had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).